Payglocal vs xPay | Best Payglocal alternative

For Indian Enterprises, SaaS companies, digital exporters, and subscription businesses, international payments are not a backend utility. They directly determine approval rates, realized revenue, FX leakage, finance workload, and ultimately growth velocity.

Two platforms commonly evaluated in this space are PayGlocal and xPay.

Both enable cross-border acceptance.

Both are built for Indian exporters.

But when evaluated across success rates, pricing, checkout coverage, FX transparency, and compliance automation — meaningful differences emerge.

This analysis focuses on the metrics that matter most to scaling businesses.

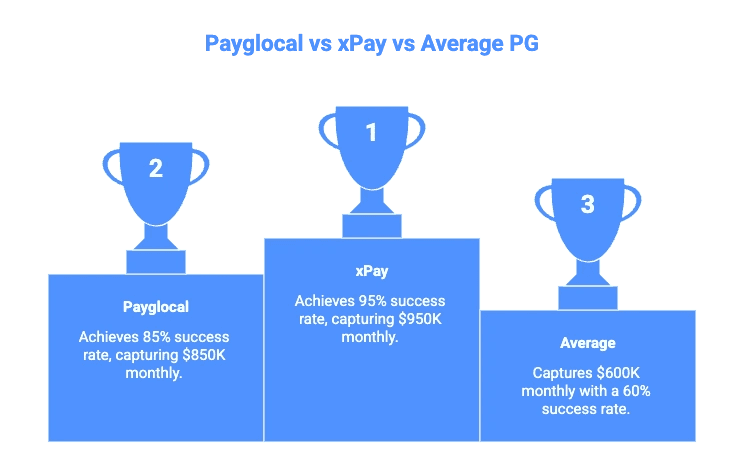

1. Success Rates: Revenue You Either Capture or Lose

Approval rate is the most underrated growth lever in international payments.

A difference of 5–10 percentage points is not marginal. It is pure revenue uplift without additional marketing spend.

PayGlocal

Average international success rate: ~80%

xPay

Average international success rate: ~95%

What does this mean in practice?

If you process $1M per month in international volume:

At 80% success → $800K captured

At 95% success → $950K captured

That is $150,000 additional monthly realized revenue

Or $1.8M annually — without increasing traffic.

For SaaS and subscription businesses, approval rate is often more impactful than pricing.

Why the difference?

xPay’s infrastructure combines:

Optimized routing

Local acquiring partnerships

Wallet + alternative method coverage

Reduced friction checkout flows

The result is materially higher authorization capture across key corridors.

Edge: xPay

2. Pricing: Effective Cost Per Dollar Processed

While success rates drive topline capture, pricing determines retained margin.

PayGlocal

Effective pricing: ~3.75% for international processing

xPay

Effective pricing: ~3.0% for international processing

At first glance, the delta seems small.

But at scale, it compounds.

On $1M monthly volume:

PayGlocal at 3.75% → $37,500 in fees

xPay at 3.0% → $30,000 in fees

That is $7,500 saved monthly

Or $90,000 annually

Now combine:

Higher success rate + Lower fee = double impact

When you model both together:

Metric | PayGlocal | xPay |

|---|---|---|

Monthly Attempted Volume | $1,000,000 | $1,000,000 |

Approval Rate | 80% | 95% |

Captured Revenue | $800,000 | $950,000 |

Processing Fee | 3.75% | 3.0% |

Net After Fees | $778,125 | $921,500 |

That is a $143,375 monthly difference in net revenue

Or over $1.8M annually.

Even if your volume is smaller, the margin uplift remains structurally meaningful.

Edge: xPay

3. Payment Method Coverage & Checkout

PayGlocal provides:

International card acceptance

20 Global payment methods

Recurring billing

Multi-currency support

xPay provides:

International cards

45+ global and local payment methods like Apple Pay, wallets, BNPL options and CC EMI

Multi-currency pricing

Brand-able checkout

Subscription-ready infrastructure

Virtual bank accounts

For SaaS businesses selling in the US, EU, and emerging markets, payment method diversity often correlates with approval lift.

xPay integrates bank transfers, wallets, cards, and subscriptions into one unified stack.

Edge: xPay (broader infrastructure)

4. Virtual Accounts & Bank Transfers

Both platforms support multi-currency account collections.

xPay additionally offers:

Virtual USD, GBP, EUR accounts

1% pricing on bank transfer collections

Zero FX markup

Automated FIRC

Export-ready documentation

For businesses with mixed B2B + self-serve flows, having both bank transfer rails and global checkout under one integration simplifies operations.

Edge: xPay

5. FX Transparency & Revenue Predictability

International businesses often underestimate FX leakage.

xPay provides:

Live mid-market FX

Zero hidden markup

Real-time visibility on dashboard

Transparent FX improves forecasting and protects margin.

Edge: xPay

6. Compliance & Finance Ops

PayGlocal:

Provides FIRA/FIRC post settlement

RBI-regulated infrastructure

PA-BC Compliant

xPay:

Instant automated FIRC

Purpose code tagging

GST/LUT-ready documentation

Streamlined export workflows

PCI-DSS Compliant

Settlement via PA-CB channels

For finance teams handling zero-rated GST and monthly filings, automation reduces internal operational cost.

Edge: xPay

Where PayGlocal Still Makes Sense

PayGlocal may be appropriate if:

Your approval rates are already strong

Your business model is primarily straightforward card acceptance

You are earlier in international scale

It is a credible cross-border platform.

Where xPay Becomes the Stronger Strategic Choice

xPay becomes compelling when:

You are scaling on high volumes or subscription revenue

Approval rates directly affect ARR

You want both virtual accounts and global checkout

You want lower effective processing cost

You care about FX transparency

You want automated export compliance

You are optimizing net revenue, not just gateway cost

Final Verdict

Both PayGlocal and xPay are capable cross-border payment platforms.

xPay consistently delivers stronger revenue outcomes for high-growth exporters.

For companies processing meaningful international GMV, the difference is not incremental.

It is structural.

FAQ's

What is PayGlocal and how does it help Indian businesses accept international payments?

PayGlocal is a cross-border payments platform that enables Indian merchants to accept international payments through global payment methods (cards, wallets) and multi-currency collections. It supports international checkout, recurring billing, and multi-currency accounts, and is RBI-authorised to operate cross-border payment aggregation services.

How does PayGlocal’s international payment pricing work?

PayGlocal publicly lists standard pricing for international acceptance at around 3.75% for card transactions and 0.25% for multi-currency account collections, with options for customized pricing depending on volume and product mix.

What payment methods and checkout options does PayGlocal support?

PayGlocal supports major global debit and credit cards and 20+ international payment methods such as Trustly, Sofort, Grabpay and Klarna. Merchants can accept payments via hosted checkout, payment links, buttons, and automated recurring billing.

What is the role of multi-currency accounts in PayGlocal?

PayGlocal’s multi-currency accounts allow businesses to receive funds in multiple global currencies, providing faster and more efficient settlement than traditional banks. Merchants can collect in 33+ currencies from customers in 180+ countries.

How does PayGlocal ensure secure and compliant cross-border transactions?

PayGlocal operates under RBI’s Payment Aggregator – Cross Border – Inward & Outward (PA-CB-I&O) authorisation, enabling compliant international payment flows. It also uses encryption, fraud prevention, and secure checkout practices to protect customer data and reduce payment risk.

What is the difference between xPay and PayGlocal for international payment acceptance?

Both xPay and PayGlocal enable Indian businesses to collect cross-border payments, but they differ in core capabilities. PayGlocal focuses on international card processing and multi-currency account collections with flat pricing and RBI-regulated compliance. xPay offers all of that plus broader payment method coverage (45+ methods), virtual bank accounts, subscription billing, higher approval rates (~95% vs ~85%), and integrated export compliance automation — offering both global checkout and bank transfer rails from one platform.

Which platform has better international success rates: xPay or PayGlocal?

International approval rates directly impact realized revenue for exporters and SaaS companies. In comparative usage patterns, PayGlocal’s average international success rate is ~85%, whereas xPay’s routing logic, local acquiring partnerships, and broader method coverage support ~95% success rates. Even a 5–10% improvement in approval can translate into significant incremental revenue without increasing traffic or CAC.

How do xPay and PayGlocal compare on pricing and cost for international payments?

Pricing differences matter for net revenue, especially at scale. PayGlocal’s standard international card processing fee is around 3.75%, while xPay’s effective pricing for similar flows is approximately 3.0%. On $1M in monthly international volume, this fee delta alone can save tens of thousands of dollars annually. Combined with higher success rates and improved FX transparency, xPay’s model often results in better retained margin for fast-scaling exporters.