Compliance, KYC, AML, and Regulatory Challenges in International Payments

A Technical Guide for Indian Businesses Scaling Globally

As Indian businesses expand into global markets, accepting international payments is no longer just a growth lever. It is a regulatory commitment.

Behind every successful cross-border transaction lies a layered ecosystem of compliance controls, banking oversight, anti-money laundering safeguards, data protection mandates, and central bank regulations. Ignoring or misunderstanding these requirements can result in settlement delays, frozen funds, penalties, or permanent account shutdowns.

This guide breaks down:

How compliance works in international payments

KYC and AML obligations across jurisdictions

Regulatory frameworks affecting Indian exporters

Common risk and compliance pitfalls

How modern payment infrastructure simplifies global compliance

1. Why Compliance Is the Foundation of Cross-Border Payments

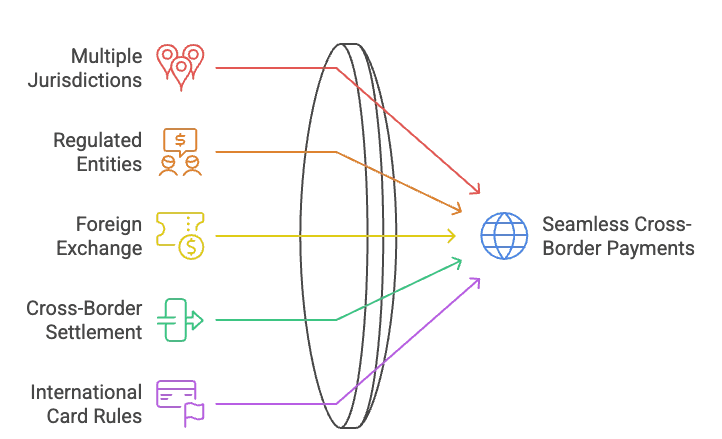

Cross-border payments differ fundamentally from domestic transactions because they involve:

Multiple jurisdictions

Multiple regulated entities

Foreign exchange conversion

Cross-border settlement rails

International card network rules

Each layer introduces additional regulatory exposure.

When an Indian merchant accepts a payment from a customer in the US, EU, UAE, or Singapore, the transaction typically touches:

A card network such as Visa or Mastercard

An acquiring bank in the payment processing jurisdiction

A foreign exchange channel

A remittance pathway governed by Indian foreign exchange regulations

Domestic settlement into an Indian bank account

Every participant is regulated. Compliance is not optional. It is infrastructural.

2. Understanding KYC in International Payments

What Is KYC?

Know Your Customer is the regulatory process through which financial institutions verify the identity, legitimacy, and risk profile of a business or individual before enabling financial services.

In cross-border payments, KYC applies to:

Merchants

Beneficial owners

Directors and key management personnel

In some cases, high-risk customers

Why KYC Is Stricter for International Payments

Cross-border transactions carry elevated risks of:

Money laundering

Terror financing

Trade-based fraud

Sanctions violations

Tax evasion

Therefore, acquiring banks and payment providers must conduct enhanced due diligence.

Typical KYC Requirements for Indian Exporters

Certificate of Incorporation

PAN and GST details

Board resolution

Ultimate Beneficial Owner declaration

Bank account verification

Nature of business and website review

Export classification details

In India, payment aggregators and banks operate under the supervision of the Reserve Bank of India.

RBI guidelines mandate strict onboarding and monitoring requirements for payment intermediaries.

Failure to provide complete documentation often leads to onboarding delays or outright rejection.

3. AML and Transaction Monitoring: What Happens After Onboarding

Onboarding is only the beginning.

Anti-Money Laundering compliance continues throughout the merchant lifecycle.

Core AML Components

Sanctions screening against global watchlists

Ongoing transaction monitoring

Suspicious activity reporting

Velocity and behavioral anomaly detection

Chargeback and fraud analysis

Globally, AML standards are shaped by the Financial Action Task Force.

Financial Action Task Force

FATF provides international AML recommendations adopted by over 200 jurisdictions.

Payment providers must implement real-time monitoring systems to:

Detect structuring

Flag unusually large or inconsistent transactions

Monitor high-risk geographies

Identify suspicious refund patterns

If anomalies are detected, accounts may be temporarily suspended pending review.

4. Regulatory Frameworks Governing International Payments

4.1 Indian Regulatory Landscape

Indian exporters receiving international payments must comply with:

FEMA guidelines

RBI Master Directions on export proceeds

Authorized Dealer Category I banking norms

Payment Aggregator cross-border regulations (PA-CB)

Under FEMA, export proceeds generally must be realised within prescribed timelines, subject to sectoral exemptions.

Settlement into India must occur through RBI-regulated channels.

4.2 Global Regulatory Considerations

Depending on where acquiring occurs, merchants may indirectly fall under:

US financial regulations

EU PSD2 standards

UK FCA rules

Singapore MAS guidelines

UAE Central Bank compliance norms

For example:

Financial Conduct Authority regulates payment institutions in the UK.

Monetary Authority of Singapore oversees payment services under the Payment Services Act.

When your payment partner uses licensed foreign entities, compliance obligations extend across these frameworks.

5. Merchant of Record Models and Regulatory Structuring

A Merchant of Record structure centralizes compliance under a regulated foreign entity.

Under this model:

The foreign entity contracts with the end customer

Licensed acquirers process transactions locally

FX conversion occurs at the regulated banking level

Funds are remitted to India through compliant channels

This model is widely used by global platforms such as:

Stripe

dLocal

Properly structured global acquiring reduces:

Cross-border decline rates

Regulatory ambiguity

Settlement unpredictability

Excessive intermediary banking fees

6. Key Compliance Challenges for Indian Businesses

6.1 High Decline Rates Due to Risk Filters

International issuers apply stricter fraud checks for cross-border transactions.

If compliance signals are weak, transactions fail at authorization.

6.2 Chargeback Exposure

Cross-border card transactions carry elevated chargeback risk.

Excessive chargeback ratios can trigger:

Monitoring programs

Increased reserve requirements

Acquirer termination

6.3 Sanctions and Restricted Geographies

Payments involving sanctioned jurisdictions can lead to immediate account suspension.

Providers must screen against OFAC and other global sanctions lists.

6.4 Documentation Gaps

Incomplete export classification, vague business descriptions, or website inconsistencies often lead to compliance escalations.

6.5 Data Protection Requirements

Cross-border payments also intersect with:

PCI DSS standards for card security

Data localization considerations

GDPR exposure when dealing with EU customers

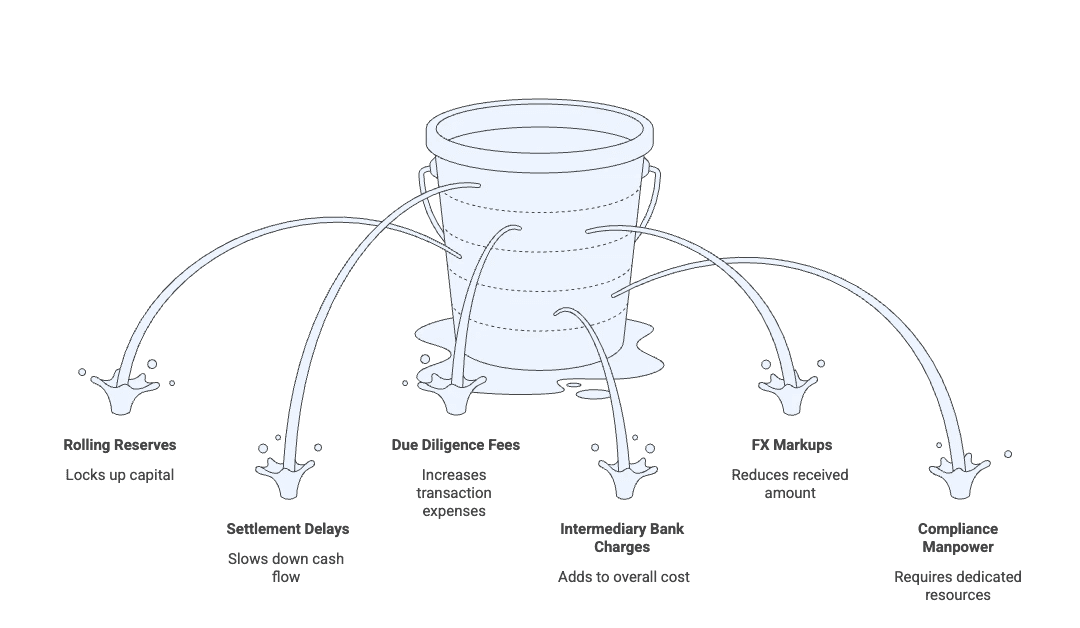

7. Hidden Regulatory Costs in Cross-Border Payments

Compliance impacts cost structures through:

Rolling reserves

Settlement delays

Enhanced due diligence fees

Intermediary bank charges

FX markups

Compliance manpower

Many merchants only evaluate processing rates but overlook regulatory friction as a cost multiplier.

8. How Modern Infrastructure Reduces Compliance Friction

Advanced cross-border payment platforms integrate:

Automated KYC workflows

Real-time sanctions screening

Smart transaction monitoring

Dynamic 3DS trigger controls

Geo-optimized routing

Multi-currency settlement

For Indian businesses, this translates into:

Faster onboarding

Higher authorization rates

Lower regulatory exposure

Compliant INR remittance

9. Best Practices for Managing International Payment Compliance

Maintain updated corporate documentation

Clearly describe business models and refund policies

Implement transparent checkout disclosures

Monitor chargeback ratios monthly

Avoid high-risk geographies without regulatory clarity

Partner with globally licensed processors

Ensure PCI DSS compliance for card handling

Maintain export reconciliation records

Compliance is an operational discipline, not a one-time checklist.

10. The Future of Cross-Border Compliance

Regulators worldwide are increasing scrutiny on:

Digital services exports

Subscription-based global businesses

BNPL cross-border flows

Crypto-linked transactions

Real-time transaction monitoring and AI-driven compliance engines are becoming standard infrastructure.

Businesses that embed compliance into product architecture scale faster and face fewer disruptions.

FAQs

What is the difference between KYC and AML?

KYC focuses on verifying identity and legitimacy at onboarding. AML involves ongoing monitoring to detect suspicious activity.

Why are cross-border transactions more heavily monitored?

They carry higher risk of money laundering, sanctions violations, and fraud due to jurisdictional complexity.

Can funds be frozen during compliance review?

Yes. If transactions trigger AML alerts or sanctions screening issues, temporary restrictions may apply.

Do Indian businesses need to comply with foreign regulations?

Indirectly, yes. If payments are processed via foreign acquiring entities, those entities must comply with their local regulators.

How can merchants reduce compliance-related declines?

Improve checkout transparency

Enable 3DS intelligently

Maintain low chargeback ratios

Use geo-optimized acquiring

Keep documentation current

What happens if chargeback ratios exceed thresholds?

Card networks may place merchants in monitoring programs, leading to higher fees or termination risk.